In budget 2014, the Government increased the holding period of debt fund units (for the resulting gains to be qualified as long term capital gains) from 1 year to 3 years.

This gave birth to new category of funds such as equity savings funds and arbitrage funds. These types of funds may have been around before 2014 too. However, such funds caught retail investor attention after 2014 only.

I have written about arbitrage funds in an earlier post. In this post, I will talk about equity savings funds.

Before moving on to equity savings, let’s talk briefly about taxation of mutual funds.

Taxation of Mutual Funds

In case of debt funds, short term capital gains (holding period <= 3 years) are taxed at investor’s marginal tax rate. Long term capital gains (holding period > 3 years) are taxed at 20% after indexation. Before July 2014, the holding period (for long term capital gains) was just 1 year.

On the other hand, in case of equity funds, short term capital gains (holding period <=1 year) are taxed at flat 15% while long term capital gains (holding period > 1 year) are exempt from tax.

You can see the tax treatment is quite favorable for equity funds, especially for redemption after 1 year and before 3 years.

It is this difference in holding period (for long term capital gains) between equity and debt funds has given birth to such categories as equity savings fund and arbitrage funds.

For a fund to qualify as an equity fund, it must invest at least 65% of the investible funds must be invested in equity shares (Clause 10(38) of the Income Tax Act).

Equity Savings Funds and Arbitrage Funds do just that. Such funds make sure that at least 65% are invested in equity shares so that the fund qualifies as an equity fund from the perspective of taxation.

How do Equity Savings funds reduce equity exposure?

Just like an arbitrage fund does. Equity Savings funds reduce net equity exposure by taking short position in derivatives market.

With arbitrage funds, the aim is to hedge the entire equity position. Hence, the returns are in line with debt funds.

With Equity Savings funds, there is typically a net long position in equity (20%-40%). This is quite unlike arbitrage funds. Arbitrage funds do not keep a net long equity position. Everything is hedged.

Not so in equity savings funds.

Consider equity savings funds more like Monthly Income plans (MIPs).

MIPs typically take up to 10-25% exposure in equities. However, MIPs do not do smart jugglery to qualify as an equity fund. Hence, the tax treatment is the same as a debt fund.

In case of equity savings funds, since at least 65% in invested in equity shares, the tax treatment is same as that of equity funds. Income tax department is not concerned about the net long equity position, which is much less due to shorts in derivatives market.

To sum up,

Arbitrage Funds invest only in Equity Arbitrage opportunities and debt instruments. There is no net long equity exposure. Tax Treatment as an equity fund.

MIPs = Equity + Debt (equity exposure ranges between 10-25%). There is net long equity exposure. Tax treatment as a debt fund.

Equity savings fund = Equity + Equity Arbitrage + Debt. Total equity investment is greater than 65%. Net equity exposure is much less. Tax Treatment as an equity fund.

With equity savings fund, there is potential for capital appreciation. At the same time, there is potential for capital loss too.

Equity Savings Funds are quite different from Balanced Funds

Equity Savings Funds may get clubbed under wrong categories.

At ValueReasearch, these funds are grouped under Equity-Hybrid funds. Balanced funds also fall in the same category.

VRO clubs ICICI Prudential Equity Income Fund and ICICI Prudential Balanced Fund under Equity-Hybrid Funds.

However, if you dig deeper, these two funds are quite different.

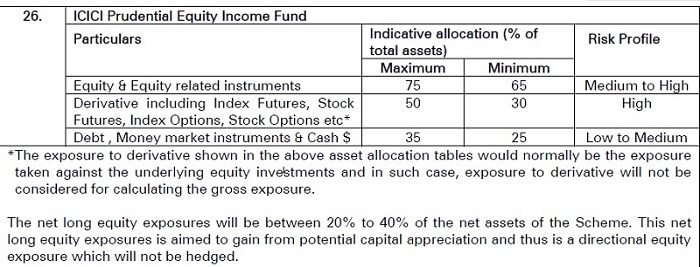

ICICI Prudential Equity Income Fund (Equity Savings Fund)

I have picked up some excerpts from Scheme Information Document for ICICI Prudential Equity Income Fund.

The Scheme seeks to generate regular income through investments in fixed income securities and using arbitrage and other derivative Strategies. It also intends to generate long-term capital appreciation by investing a portion of the Scheme’s assets in equity and equity related instruments.

So, the net long equity exposure (unhedged) will be between 20% to 40% of the net assets.

Benchmark also tells a lot about this fund. The benchmark is Crisil Liquid (40%) + Nifty (30%) + Crisil Short Term Bond (30%).

ICICI Prudential Balanced Fund(Balanced Fund)

Let’s look at investment objective for ICICI Prudential Balanced Fund.

To generate long-term capital appreciation and current income by investing in a portfolio that is invested in equities and equity related securities as well as in fixed income securities.

You can see there is no arbitrage position (using derivatives). Benchmark is Crisil Balanced Fund Index.

Comparing performance of ICICI Prudential Equity Income Scheme with ICICI Prudential Balanced Fund may not be an apple to apple comparison. Risk and return profiles will be extremely different.

You can expect a balanced fund to outperform Equity Savings Fund when the equity markets are doing well.

On the other hand, Equity Savings Funds are likely to perform better when the equity markets perform badly.

What are the issues?

Nomenclature is a big issue. Some AMCs might call such funds Equity Savings funds while others may call Equity Income Funds. There can be other fancy names too.

The other big problem is that equity savings funds can be very different from each other. For instance, there is no rule which says that net equity exposure will only be between 20-40%. AMCs can get very creative.

Other schemes may choose to take higher or lower equity exposure limit.

It may not be easy for a lay investor to understand what he is buying into. Though it is important to read Scheme Information document for every fund you plan to invest in, it is extremely important for equity savings funds and arbitrage funds.

PersonalFinancePlan Take

Apart from favorable tax treatment, there is nothing special about equity savings fund. As mentioned before, the primary reason for existing of such funds is the favorable tax treatment of equity funds (as compared to debt funds).

You can easily generate a similar product (from the perspective of taxation) using a mix of a balanced fund and an arbitrage fund. If you are not keen on arbitrage funds, you can add a liquid fund. Of late, arbitrage funds have struggled but may still provide better tax-adjusted returns than liquid funds for investors in the higher tax brackets.

You can look at Equity savings funds for medium term goals (5-10 years). It can be an alternative to a Monthly Income Plan (or any other debt hybrid product).

However, focus on the net equity exposure. Net equity position is likely to be much higher for an Equity Savings fund (as compared to MIP) and hence such funds will be more volatile than MIPs. Tax treatment is favorable too for an equity savings fund.

If you plan to invest in an equity savings fund, do go through the scheme information document to understand fund’s investment objective and mandate. Do not just fall for the name.

Remember, an Equity Savings fund has a net long equity exposure and is not meant for short term goals. It is not an alternative for liquid or short term debt funds.

4 thoughts on “PFP Primer: What are Equity Savings Funds?”

It’s nice to hear you but you did not clarify the kind of return we can expect from these type of funds. Should we keep our expectations around 11-12% CAGR P.a.?

Such funds provide market linked returns. Since exposure to equity is quite limited, it is difficult to expect such high returns from equity savings funds in the long term.

Hi Deepesh,

For bigger portfolios, can BAF and Equity Savings fund can be considered as ‘Low Risk’ Equity portion (though they have risks, the SD seems to be low compared to Nifty 50 et al)? Never a fan of hybrid but with recent tax changes, thinking of having a slightly reduced debt portion and instead of pure equity, want to have safe hybrid funds for this incremental equity allocation.

Thanks.

Hi Thiyagu,

Yes, the recent tax changes have tilted the scales in favour of hybrid funds. Investors may opt for such products for lower taxation (despite higher risk).

But not an apples-to-apples comparison.

These products carry much higher risk than pure debt funds.

We just need to go back and see how these funds performed in March 2020.

Interesting thought. Quite possible many are already doing this. But need to appreciate risk.