Mis-selling is not uncommon during the sale of financial products. Many of us buy investment products with a false impression of the product. While salespersons/advisors are the culprits, we, the investors must share the blame too. We rely too much on the illustrations and pamphlets shared and do not care to look beyond those fancy documents.

Advisors/salespersons, on their part, come with aggressive illustrations, knowing full well that the investors will not fully appreciate the risks on their own. It is the responsibility of the salesperson to explain the product properly. However, when the focus is just to make a sale, such considerations recede to the background. They tout the good features but remain silent about the risks. Sometimes (not always), it is also deliberate.

In this post, I will share such an instance of mis-selling in the SBI Life Smart Elite plan. I will discuss an illustration that was shared with one of my NRI clients. He was impressed and shared the illustration with me. While we decided not to invest in the plan, I thought of writing about what such sales illustrations conveniently hide and how they mislead the investors.

Note that this is not a commentary on SBI Life-Smart Elite plan. I do not intend to review the plan or discuss its merit or demerits. This post is a commentary on how ULIPs are mis-sold in our country. This can apply to any ULIP or any other investment product in the country.

I begin with some features of the SBI Smart Elite ULIP and discuss the issues with the illustration subsequently.

SBI Life – Smart Elite Plan comes in 2 variants

1. Gold Plan

Type-I ULIP. In the event of demise of the policyholder, the nominee gets the higher of Sum Assured or the Fund Value (your accumulated wealth in the plan). Therefore, Sum-at-risk goes down as the fund value increases over the years. Sum-at-risk is the amount insurance company pays from its pocket in the event of policyholder demise.

For instance, if the Sum Assured is Rs 10 lacs and fund value has grown to Rs 2.5 lacs, the Sum-at-risk goes down to Rs 7.5 lacs.

Since mortality charges are linked to the Sum-at-risk, the impact of mortality charges goes down over the years. Mortality charge is the cost you incur for getting life cover in the ULIP.

While the mortality charge per unit of Sum-at-risk goes up with age, the Sum-at-risk goes down with the increase in fund value. The net impact is the reduced impact of mortality charges. In fact, when the fund value is higher than the Sum Assured, there shall be no mortality charge deducted.

2. Platinum Plan

Type-II ULIP. In the event of demise of the policyholder, the nominee gets the Sum Assured + Fund Value. Therefore, the Sum-at-risk remains constant over the years.

For instance, if the Sum Assured is Rs 10 lacs and fund value has grown to Rs 2.5 lacs, the Sum-at-risk will still be Rs 10 lacs. It will be Rs 10 lacs for the entire duration of the policy.

Thus, the impact of mortality charges goes up over the years. The Sum-at-risk is constant. The mortality charge per unit of Sum-at-risk goes up with age.

Everything else being the same, an investor will earn higher returns in a Type-I ULIP. Therefore, if you must invest in a ULIP for investment (and not insurance), you must invest in a Type-I ULIP.

Read: How to select the Best ULIP for your portfolio? (If you must invest in a ULIP)

My client didn’t get to that point. So, we don’t know what he was being sold. Given that not everybody understands the nitty-gritties of such products, it is usually up to the discretion of the sales representative. The prospect merely looks at the illustration numbers (which are not guaranteed) and trusts the salesperson.

Let us give the salesperson the benefit of doubt. Since my client was interested only in an investment plan, let us work with the assumption that the advisor wanted to sell only the SBI Life- Smart Elite-Gold plan (Type-I ULIP).

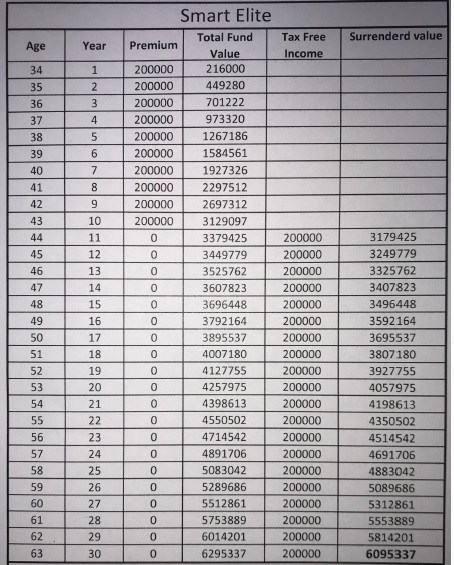

SBI Life Smart Elite: The Illustration

First thing to notice is that is not an official illustration. Usually, that will happen when the illustrations are blatantly wrong.

Where is the mis-selling?

- The illustration seems to give the impression that the returns are guaranteed. My client was under this impression. That is not the case. SBI Life-Smart Elite is a ULIP. The returns are not guaranteed. The returns can be higher or lower.

- You can see that the illustration is for a 34-year-old (at the time of entry). My client is close to 50. Again, we know, everything else being the same, the returns for the 50-year-old investor will be lower than the 34-year-old investor. Does not matter if they invested on the same day, had the same policy tenure, and invested in the same funds. A higher entry age means higher mortality charges over the policy tenure. The higher charges eat into the returns. This aspect was never communicated to the prospect. Even if we trust the calculations in the illustration, a 50-year-old investor will earn a lower return.

- The policy does not really have an income option. Therefore, Rs 2 lacs per annum from the 11th year until the end of the 30th year does not come as a policy feature. However, there is an option of partial withdrawals. After the end of 5th policy year, you can make partial withdrawals. So, you can use these partial withdrawals to generate a source of income for yourself. However, the number of partial withdrawals is limited to a maximum of 10 over the entire policy term. In the illustration, 20 partial withdrawals of Rs 2 lacs each are shown. This is not allowed

Where is the problem with calculations in the Illustrations?

#1 I could regenerate the entire illustration using a gross investment return of 8% p.a. However, what eventually you get are the net returns. You earn the returns after all the charges (mortality, policy administration etc) have been deducted. These charges have not been adjusted in the illustration. Your net returns will be much lower than gross returns. No such explanation was offered to the prospect.

Read: How various charges eat into ULIP returns?

#2 Note that SBI Life-Smart Elite is not a low cost ULIP. Quite an expensive one in fact. The premium allocation charge itself is 3% of annual premium for each of the first five years.

#3 I went to SBI Life website and tried to reproduce the numbers. 34-year-old, Premium payment term: 10 years, Policy Term: 30 years, Gold variants. Here is the output.

#4 What SBI shows are the net returns (and not gross returns). It shows the tentative maturity value assuming a gross investment return of 4% and 8% p.a. It does not consider partial withdrawal of Rs 2 lacs per year from the 10th year. At 8% p.a. gross return, it ends with 94.58 lacs. If you remove the Rs 2 lacs withdrawal per year from our calculations (or as per illustration), we would have ended with Rs 1.46 crores.

Now, that is a remarkable difference. SBI Life shows maturity value of 94.58 lacs at 8% p.a. gross return while our calculation (illustration) shows a maturity value of Rs 1.46 crores.

Why this difference of almost Rs 51 lacs?

This is the impact of ULIP charges. ULIP charges will eat this Rs 51 lacs over the 30 years.

Hence, the gross yield of 8% p.a. (which would have given you Rs 1.46 crores at the end of 30 years) gets you Rs 94.58 lacs (a net yield of 6.22% p.a.)

Clearly, this was not communicated to the prospect.

#5 Additionally, there is an error in the calculations after the 10th year. While Rs 2 lacs is paid out every year from the end of 11th year, the returns for the Rs 2 lacs are still counted in the next year. Effectively, adding Rs 16,000 in returns every year (Rs 2 lacs X 8%). This is clearly wrong. This leads to a difference of Rs 6.63 lacs in the final value. The final year value should have been Rs 56.32 lacs. It is shown as 62.95 lacs. Note that all these calculations (in the illustration) are at 8% gross return and ULIP charges have not been considered.

What should you do?

Before investing, understand what you are getting into. And this applies to all the investments and not just ULIPs. It applies to mutual fund investments too. Mis-selling happens in MF investments too.

Do note just go by what your salesperson offers. The numbers are usually embellished. The best-case scenarios may be presented.

Excel is a funny thing. You can make minor changes to your data or return assumptions and show whatever you want.

In the case of ULIPs, the IRDA mandates insurance companies to provide tentative maturity values at gross investment yields of 4% and 8%. You can do these calculations on the insurer website. Pick up these maturity values for your case. Plug in the premium payments and the maturity value in the IRR function and figure out the net yield. Alternatively, you can compare the maturity value on the insurer website with your own calculation at 8% gross yield and see the impact of charges.

About SBI Smart Life, the SBI Life-Smart Life product page of SBI Life website mentions “For the privileged few who seek maximum from life”. Trust me many investors fall for this nonsense messaging. With the egos massaged, at least one inhibition is out of the way. While the intent is not to review the SBI Life Smart Elite plan, I must say that it is an awfully expensive plan and must be avoided. I see no merit in this plan.

Disclosure: I structure equity portfolios for my investors using mutual funds. Hence, you can expect my bias towards mutual funds. I do not deny that either. For an objective analysis of ULIP vs Mutual Funds debate, refer to this post.

Read: ULIPs Vs Mutual Funds

Additional Links

SBI Life Smart Elite product page on SBI Life website

7 thoughts on “SBI Life Smart Elite: How do you mis-sell the plan?”

People simply comments against ulips..

I’m a person who is highly benefited from SBI Life ulips.. It simply depends on the plan we select.

Don’t go blindly on all without good observation.. There are professional agents who sell the plans with integrity.

It is nonsense to go for these kind of public comments in base on one two cases which are represented as misselling.

Excellent review.sbi life people are frauds and hide the facts and figures to inocent investors

Yes sbi smart elite is very bad policy

I started 2lacs per year in this policy l calculated total charges

First year charges 22 thousand from 2 lack

Second year charges 24 thosand

Third year charges 27 thosand total

3 year 27 k

4th year 30 k

5th year 33k total chages

There are too many hiden chargrs in this policy

Thanks for your inputs.

Sbi Life smart elite LP is not good policy as per they told and there’s no response from them.

correct

please don’t believe sbi bank employee they misguide NRI customer

they forcing to invest sbi link policy for getting there commission only.