You just received your annual bonus. You also run a home loan.

You have 2 options.

- Use the bonus (or any lump sum) amount to repay the loan. OR

- Invest the amount and potentially earn better returns than the home loan interest rate.

What should you do with your bonus money?

Like everything in personal finance, there is no black and white answer to this question.

My usual stance in the “Invest or Prepay” debate

Try to bring the outstanding loan amount to comfortable levels by making loan prepayment. “Comfortable” is subjective. Once the home loan amount is comfortable, you can choose depending on your preference and risk appetite.

And there are reasons for this.

Firstly, you must pay the loan installment but there is no guarantee of good returns from your investments. Many investors underappreciate risk and make insipid choices with their investments. By prepaying the home loan, you at least save the home loan interest. And the interest saved is interest earned.

Secondly, do not discount the issues that your investment behaviour can bring up. Equity investments are volatile. A difficult journey can put you under pressure and you can make mistakes. You might make a sound investment but exit at the wrong time. In contrast, home loan repayment is a simple choice.

Finally, seeing the outstanding loan amount come down would make most people comfortable.

A simple and comfortable decision. Not the most optimal decision. Some would even call it lazy thinking. Fair enough.

Now, if we assume that you will not make bad investment choices and not be worried by volatility, how would this decision look?

Or in other words, if you had invested the bonus/lump sum and not repaid the loan, how would those decisions have looked in hindsight?

What does the data tell us?

Let us find out.

How do you decide if you did better by investing instead of prepaying?

Let us assume, instead of making the loan prepayment, you invested the amount in Nifty 50. And you revisit the choice after a period.

Did you earn better returns than the cost of the loan?

If your investment in Nifty 50 fetches higher returns than the cost of the loan consistently, investing would appear a better choice. Otherwise, loan prepayment is a better choice.

Now, you would make those investments (instead of prepayment) on different dates. So, we cannot just pick up any date for this analysis.

That’s right.

We can address this concern by looking at rolling returns data.

A rolling returns chart is simply a plot of point-to-point returns for a lookback period.

The plot for 1-year rolling return on Jan 25, 2021, will be the return over the previous 12 months (from January 26, 2020, until January 25, 2021). You can also average the rolling returns data for all the dates to get the average 1-year rolling return.

Similarly, to plot a 3-year rolling returns chart, the look-back period is 3 years. For the plot point for January 25, 2021, we look at the return from January 26, 2018, until January 25, 2021.

Analyzing rolling returns is an effective way to eliminate start date and end date bias. We can review 3-year and 5-year rolling returns.

We can look at the rolling returns chart or average rolling returns and see if the investment has done better than the cost of the loan.

But there is a problem.

What should be the cost of a home loan during the period?

- Home loan interest rates have come down since the late 90s. Just look at this data from the State Bank of India. Home loan interest rates until the 1990s were easily above 15%. Ranged from 10% to 15% during 2000-2010. Only for a brief period in 2003-2004) did interest rates fall between 8.5%-10% p.a. Until 2015, the home loan interest rates were still close to 9-10%. Hence, the recent sub-8% p.a. home loan interest rate is novel for Indian investors.

- I have considered only the SBI data and this data pertains to their best borrowers. Other banks/HFCs could have offered vastly different interest rates. Even SBI could have asked more from its less creditworthy investors.

- The home loan interest rate is not constant.

- Post-tax cost of a loan can be different for different borrowers. For a borrower in the 30% tax bracket, the effective cost of a 10% loan would be 7%. For a borrower in the 5% tax bracket, the effective cost of the same 10% loan would be 9.5% p.a.

- Not just that, the tax benefit on interest payment on home loan is capped at Rs 2 lacs (for a self-occupied property). So, if the loan is at 8%, just Rs 25 lacs loan would maximize the tax benefits. Excess interest payment does not get you any tax benefit. For the excess amount, the pre-tax cost remains the post-tax cost of the loan.

- You can get a higher tax benefit for interest payment for a let-out property (and not self-occupied property).

This is complicated.

Moreover, LTCG on equity has been exempt from tax for a considerable period (from 2004 until early 2018). Now, there is a 10% tax on LTCG.

Let us make a few assumptions

- The amount under question (for repayment or investing) won’t affect tax benefits if you use the amount for home loan repayment. For instance, for a self-occupied property, you do not get any tax benefit under Section 24 for interest paid on outstanding principal over 25 lacs (assuming an 8% rate of interest). By making the repayment, you do not bring the loan amount under Rs 25 lacs. Hence, the cost of the loan to compare against returns from equity is the pre-tax cost of the loan (or the actual loan interest rate).

- If your post-tax cost of the loan is lower than your loan interest rate, you can view the analysis accordingly.

- LTCG on sale of equity/equity funds (more than 1 lac per annum) gets taxed at 10% per annum. This reduces your realized returns from equity. For this exercise, let’s assume the tax on LTCG to be zero.

- We do not indulge in market-timing or look at valuations to invest. When available, the money is invested instantly.

How to decide the winner?

- Equity returns should be comfortably higher than the cost of the home loan. The risk must be worth it.

- Nifty 50 must have beaten the loan interest rate 70% of the time. You can choose a different threshold.

- For 2001-2010, the home loan interest rates ranged from 10-15% p.a. So, 15% is safe. Between 12% and 15% is OK. Below 12% is not good.

- For 2011-2020, the interest rates have ranged from 8-10% p.a. So, more than 12% is good. Above 10% is OK. If you get less than 10%, it is not worth it.

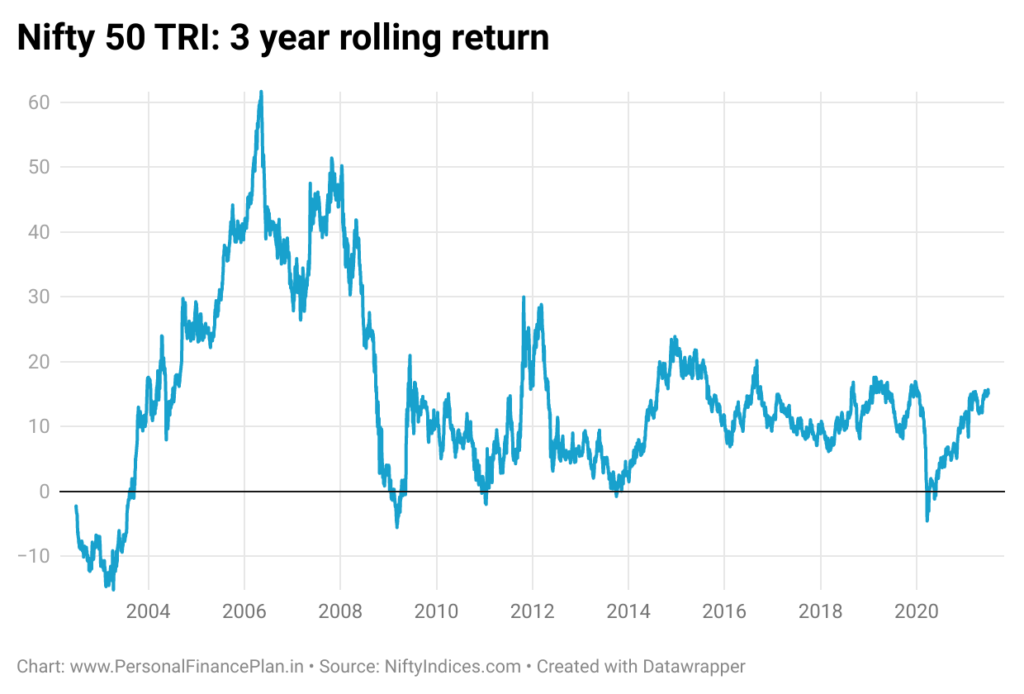

3-year rolling returns

While building up this table, I have considered the data for investments made in this period. For instance, the 3-year rolling returns data for 2001-2010 considers investments made between January 1, 2001, and December 31, 2010. For this, I have picked data for January 1, 2004, and December 31, 2013, from the rolling returns plot.

2001-2010:

Nifty 50 TRI 3-year rolling return exceeds 15% p.a. only 51.5% of the time.

>12%: 58.7% of the time

The loan interest rates ranged between 10% and 15% p.a. during the decade. You would have wanted at least better than 12% p.a.

2011-2020

>12%: 50% of the time

>10%: 67.9% of the time

The interest rates during this period were 8.5%-10% p.a.

So, you would want to earn at least 10% for the risk to be worthwhile.

In neither of the decades, do we cross our threshold of 70% (remember this threshold is artificial. You can choose a different threshold).

Note the difference in average 3-year rolling returns in the two decades. In 2001-2010, you earned 20% p.a. In 2011-2020, you earned 12.05% p.a.

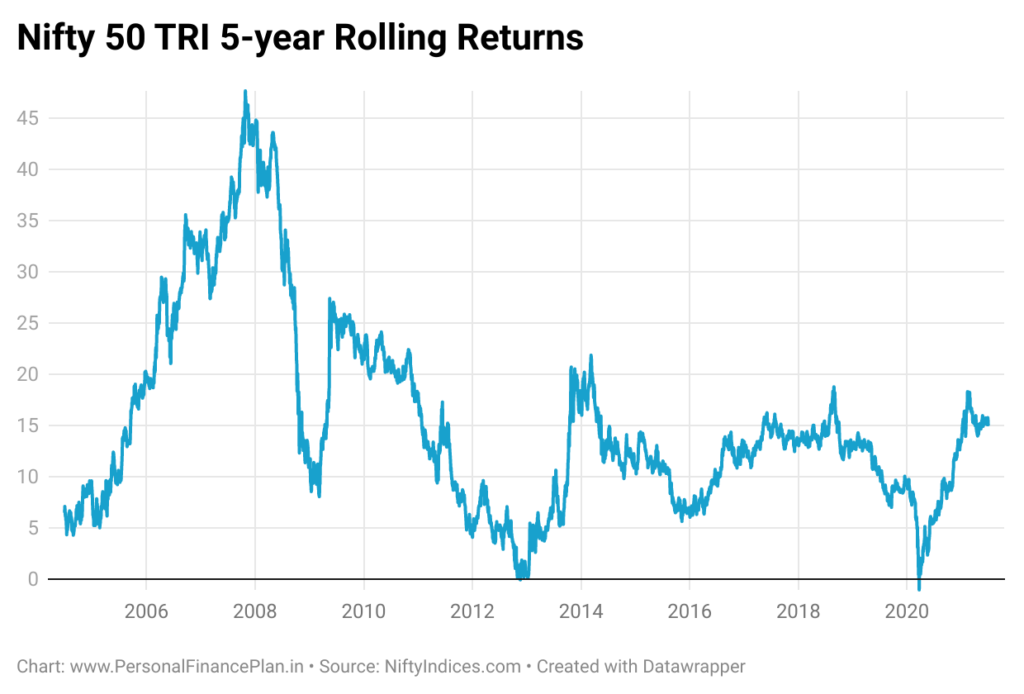

5-year Rolling returns

You are a long-term investor and want to compare against 5-year rolling returns.

2001-2010:

Nifty 50 TRI 5-year rolling return exceeds 15% p.a. only 52.9% of the time.

>12% p.a.: 64.8% of the time

The loan interest rates ranged between 10% and 15% during the decade. You would have wanted at least better than 12 p.a.

2011-2020

>12%: 54.2% of the time

>10%: 64.3% of the time

The interest rates during this period were 8.5%-10% p.a.

So, you would want to earn at least 10% for the risk to be worthwhile.

Again, lower than the threshold of 70% for either decade. Note that the threshold of 70% is artificial.

What does this mean?

The argument for investing is not very convincing. There is no overwhelming evidence (subjective) that investment (instead of prepayment) would have been a better choice. Sure, some investors would have made it work for them. However, for normal investors like you and me, we need more favourable numbers.

We must also consider:

- Uncertainty with equity investments

- Potential damage due to own behavioural biases

- Realized returns would also be lower because of taxes

However, please appreciate the impact of various assumptions. The threshold of 70% outperformance. We could have used 60% instead of 70% and investing would have appeared a better choice.

The different returns threshold for the 2 decades.

We assumed that the post-tax cost of the loan is the same as the pre-tax cost of the loan.

If the effective cost of the loan (for the repaid amount) is lower due to tax benefits, then you can consider the analysis accordingly. In that case, your return threshold can be 8% instead of 10%.

The picture is not yet complete

Why only Nifty 50?

Why not Nifty Next 50 or Nifty Midcap index or Nifty Smallcap index or any actively managed fund?

Or a hybrid or a balanced advantage fund?

Or why not a mix of moderately or negatively correlated assets (equity, gold, etc)?

Valid question.

Picking up an actively managed fund for this analysis is complicated since that brings in another level of decision-making. Hence, I am not inclined to use such funds for comparison.

For the other indices or investments, we shall try to compare them in the upcoming posts.

This post was first published on emicalculator.net.

6 thoughts on “Got surplus? Would you Prepay or Invest? What does the data tell us?”

Useful article Deepesh. Nice analysis.

Thanks Prashant!

I completely agree with the usual stance. Great analysis though and quite useful as the standard response today is just invest.

Thanks Rahul!

Thank you very much Deepesh for an excellent analysis and the simple rule is: “DEBT-FREE is Ownership which gives ‘Peace of Mind’ than Expectations from Investments which is not Guaranteed”!!

Thanks Bavan!