LIC launched a new annuity plan LIC Jeevan Shanti in September 2018.

LIC Jeevan Shanti comes in both immediate annuity and deferred annuity variants.

A point to note is that LIC already has a very popular offering in immediate annuity space (LIC Jeevan Akshay VI). LIC Jeevan Shanti is quite like LIC Jeevan Akshay. The only major difference is that LIC Jeevan Shanti also has a deferred annuity variant.

Let’s find out more about LIC Jeevan Shanti plan.

Before moving ahead, let’s try to look at the difference between an immediate annuity plan and a deferred annuity plan.

What is the difference between an immediate annuity and a deferred annuity plan?

Under an immediate annuity plan, you pay a lump sum amount once and the insurance company pays you a pension for life. The pension payment starts immediately on purchase. It does not matter how long you live. The insurance company will pay you a pension for life.

Not just that, the insurer pays you the contracted rate of interest for life (irrespective of how the interest rates move in the future). Therefore, the insurance company not only assumes the longevity risk but also the interest rate risk.

An annuity plan is a good way to cover longevity risk. By purchasing an annuity plan, you can guarantee yourself an income stream for life.

LIC Jeevan Akshay VI is an immediate annuity plan.

Under a deferred annuity plan, you make payment to the insurance company (in form of a single premium or regular premium). The money gets invested as per the investment mandate of the plan. At the end of the deferral (deferment) period, the accumulated corpus is used to purchase an immediate annuity plan.

Therefore, the pension starts at the end of the deferment period. The quantum of regular income will depend on the returns earned on your investments, your age, deferral period, annuity variant and the prevailing annuity rate

LIC Jeevan Shanti is a variant of deferred annuity plan. It is a single premium plan i.e. you have to pay the premium just once. You can defer annuity for up to 20 years. The return on your investment is guaranteed and you are also guaranteed the annuity rate at the end of the deferral period. Therefore, there is no uncertainty involved. You know upfront how you will get every year after the end of the deferral period.

By the way, LIC Jeevan Shanti comes in immediate annuity variant too. Well, you can think of an immediate annuity plan as a deferred annuity plan without a deferral period.

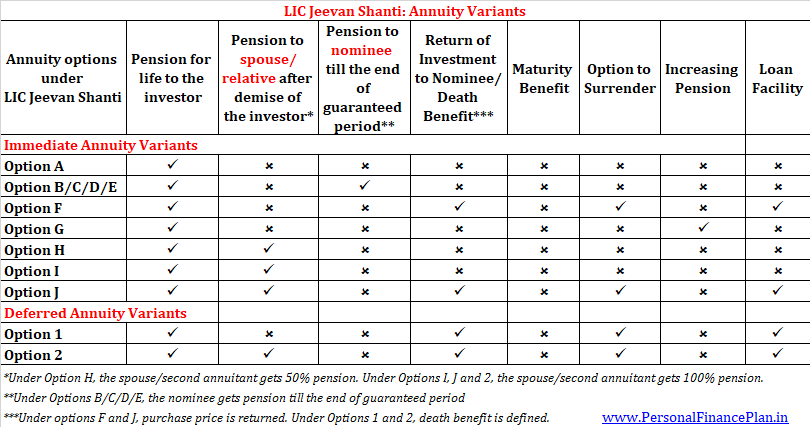

LIC Jeevan Shanti comes in 9 annuity variants (7 in immediate annuity and 2 in deferred annuity).

Read: Retirement Planning: Staggering Annuity Purchases can increase income and reduce risk

LIC Jeevan Shanti (Plan 850): Review and Salient Features

- Minimum Entry Age: 30 years

- Maximum Entry Age:

- Immediate annuity option: 100 years for Option F, 85 years for other options. Variants to be discussed later.

- Deferred Annuity option: 79 years

- Minimum Purchase Price: Rs. 1.5 lakhs subject to minimum annuity restrictions as specified below. Lower minimum purchase price permitted for NPS subscribers and for differently abled.

- Maximum Purchase Price: No Limit

- Pension Payment Frequency: Monthly, Quarterly, Half-yearly or Annual pension.

- Loan facility is available after 1 year. The loan facility is available for select variants under immediate annuity variants (Option F and J, these are variants with the return of purchase price). The loan facility is available for both the variants under deferred annuity plans.

- The loan facility is available under the aforementioned variants 1 year from the purchase of the policy. Interest on the loan amount cannot exceed 50% of the annual pension. You can get a loan up to 80% of the Surrender value.

- Surrender option is available in select variants. The surrender value will depend on the age of the annuitant (investor) at the time of surrender.

- The plan can be purchased both online and offline modes. You get 2% rebate on buying the policy online or purchasing the policy at the time of exit from NPS. Additionally, there is an incentive for the higher purchase price. (discussed later)

- GST at 1.8% is applicable on the purchase amount. If you want to invest Rs 10 lakh, you will have to pay Rs. 10.18 lac (prevailing GST rate for annuities is 1.8%)

- No medical examination is needed at the time of purchase.

You can also visit LIC’s website for more information.

Read: HDFC Life Sanchay Plus: Review

LIC Jeevan Shanti: Variants

LIC Jeevan Shanti comes in 9 annuity variants (7 in immediate annuity and 2 in deferred annuity).

Here is a snapshot to show what various variants of LIC Jeevan Shanti offer.

LIC Jeevan Shanti: Interest Rate (Annuity Rate)

For immediate annuity variants, the interest rate (annuity rate) depends on your age and the annuity variant. In the case of joint life plans (where the spouse or any other family member), the annuity rate will also depend on the age of the second annuitant.

Annuity rate will increase with the age of the investor. The insurance company pays a higher rate when its liability is lower. A 40 year old person is likely to receive pension for many more years (as compared to a 70 year old). Therefore, the annuity rate will be lower for a 40 year old and higher for a 70 year old.

For the deferred annuity variant, the annuity rate shall depend on the all the above factors. In addition, the annuity rate shall depend on the quantum of deferral period and the age of the second annuitant (in case of joint life policies).

Annuity rate will increase with the increase in the deferral period.

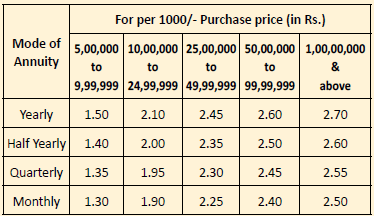

Here is the sample set available on LIC website for immediate annuity variant of LIC Jeevan Shanti. The rate is for purchase price of Rs 10 lacs.

Sample annuity rate for Deferred Annuity (Purchase price of Rs 10 lacs). The rates are for single life (and not joint life plans).

Points to Note

- The amounts mentioned in the above tables is for a purchase of Rs 10 lacs.

- The amount mentioned above is for annual pension. If you opt for monthly, quarterly or half yearly pension, the amount will be different.

- For example, a person aged 60 will receive an annual pension of Rs 90,942 rupees for life on investing Rs 10 lacs in Option i (in the table) or Option A (immediate annuity).

- Interest rate increases with your age. This does not always apply to Deferred annuity variant (discussed later).

- You will get the pension for life. You may go on to live till the age of 100 years or even 150 years. LIC will continue to pay interest as per above rates.

- This interest rate (annuity rate) may change from time to time. Before you take the plan, check at the LIC branch or on the LIC branch or on the LIC website.

- If you buy LIC Jeevan Shanti plan online, you will get 2% more pension. If a 60-year-old person invests Rs 10 lacs in option 1, he will get an annual pension of Rs 90,942 every year. Note that these rates are online rates. If you were to purchase this policy offline, you will get 2% lower pension i.e. he will get an annual pension of 90,942/102% = Rs. 89,158 per annum.

- There is a minor incentive if you invest a big amount.

- Continuing with the above example, if you invest 10 lakh rupees, then you will get a pension of Rs. 92,442 per annum instead of Rs 90,942. As you can see, the pension is higher by Rs 1,500 per annum (1.5 * 10 lacs/1000).

Let’s look at annuity variants in detail. There is nothing to differentiate between LIC Jeevan Akshay and immediate annuity variants of LIC Jeevan Shanti, except perhaps for the annuity rates. LIC Jeevan Akshay does not have a deferred annuity variant.

Therefore, I will discuss deferred annuity variants of LIC Jeevan Shanti first. For the sake of completion, I have provided illustrations for immediate annuity variants at the end of this post.

LIC Jeevan Shanti: Option 1 (Deferred Annuity)

Deferred Annuity for Single Life

Before we dig deeper, there are a couple of things that we need to understand for deferred annuity variants.

Under deferred annuity variant, you do not get anything till the end of the deferral period. Therefore, if the demise of the annuitant were to happen during the deferral period, the nominee shall get at least a bit more than the purchase price. Makes sense, right?

Therefore, under the deferred annuity variants, LIC has introduced the concept of guaranteed additions and the death benefit is more than the purchase price (at least till the end of deferment period).

What are Guaranteed Additions? (Applicable only in Deferred Annuity Variants)

Guaranteed Additions are applicable only in deferred annuity variants.

Guaranteed additions are used to calculate Death Benefit during the deferment period or after the end of the deferment period.

Guaranteed additions accrue till the end of each policy month, till the end of deferment period or death, whichever is earlier.

Guaranteed Additions per month = Purchase price * Monthly tabular annuity rate

Monthly tabular annuity rate shall depend on the annuity rate and the deferment period opted for. Monthly tabular annuity rate = (Annual Annuity Rate * 96%)/12

What is Death Benefit under Deferred Annuity variants?

Death Benefit = Higher of A and B, where

A = Purchase Price + Accrued Guaranteed Additions – Total Annuity payments made till date

B = 110% of Purchase Price (let’s ignore this for now)

Therefore, if the death were to happen during the deferment period, your nominee will get Purchase Price + Accrued Guaranteed Additions (since no annuity payments have been made yet).

The way death benefit is calculated brings in a lot of complication in the plan (Refer to the Section: The Strange Thing about LIC Jeevan Shanti). The death benefit will rise during the deferment period and start going down as annuity payments start.

The nominee can get death benefit as lump sum or can purchase an immediate annuity with the amount (annuity rate will depend on nominee’s age) or choose to receive the benefit in installments (5, 10 or 15 years). These options are not available under LIC Jeevan Akshay VI.

Now back to Option 1 (Deferred life for single annuity)

Pension Benefit: No pension till the end of the deferral period. After the end of the deferment period, the investor will get the pension for life.

Death Benefit: As mentioned above (have explained later with the help of example)

Maturity Benefit: Not applicable

Surrender Benefit: Permitted

Loan Option: Available

Illustration

A 60 year old person invests Rs 10 lakh in Option 1. The total outgo will be Rs 10.18 lacs (inclusive of GST).

The corresponding value in the table for the age of 60 and Option 1 (deferred annuity, 20 years) is 149,592.

You will not get anything for the first 20 years. After the end of the deferment period (20 years), you will get this pension of Rs 149,592 per annum for life.

Every month till the end of deferment period, the guaranteed addition will accrue to your policy at the rate of (149,592*96%)/12 = Rs 11,967 per month.

Therefore, if the death happens after 10 years (before the end of deferment period), the nominee will get Rs 10 lacs + 120 months * 11, 967 = Rs 24.36 lacs.

If the annuitant survives the deferment period, the policy would have accumulated guaranteed additions worth Rs 28.72 lacs.

If the investor passes away at the age of 85 (let’s say), the investor would have got annuity payments for 5 years. At the time of demise, the nominee will get

Rs 10 lacs + Rs 28.72 lacs (accrued Guaranteed Additions) – 5*1.49 lacs (annuity payments already made) = Rs 31.24 lacs. The nominee can choose to receive the death benefit as lumpsum, immediate annuity or installments, as per his/her choice.

LIC Jeevan Shanti: Option 2 (Deferred Annuity)

Deferred Annuity for Joint Life

The only difference between Option 1 and Option 2 is that, under Option 2, the pension continues to the second annuitant too. And death benefit is payable only after both the annuitants have passed away.

The second annuitant can be spouse, sibling or any lineal ascendant or descendant (grandparents, parents, children, grandchildren)

Additionally, the annuity rate will also take the age of the second annuitant into account.

Pension Benefit: No pension till the end of the deferral period. After the end of the deferment period, the investor will get pension for life. After the demise of the investor, the second annuitant will get the same pension for life. If the second annuitant predeceases the investor, the pension will stop after the demise of the investor.

Death Benefit: Death benefit is payable after both the annuitants have passed away. The calculation of death benefit is same as under Option 1.

Maturity Benefit: Not applicable

Surrender Benefit: Permitted

Loan Option: Available

Illustration

A 60 year old person invests Rs 10 lakh in Option 2. The total outgo will be Rs 10.18 lacs (inclusive of GST).

The second annuitant’s age is 50. The second annuitant’s age also affects your annuity rate.

The annuity rate will be (deferred annuity, 20 years) is 216,036.

You will not get anything for the first 20 years. After the end of deferment period (20 years), you will get this pension of Rs 216,036 per annum for life.

After you, the second annuitant (spouse/relative) will get pension for life. If second annuitant dies before you, the pension will stop after your demise. The nominee will not get any pension.

Every month till the end of deferment period, the guaranteed addition will accrue to your policy at the rate of (216,036*96%)/12 = Rs 17,282.

In this case, the death benefit is payable to nominee once both the annuitants die.

Therefore, if the last surviving annuitant after 10 years (before the end of deferment period), the nominee will get Rs 10 lacs + 120 months * 17,282 = Rs 30.73 lacs.

If any of the annuitants survive the deferment period, the policy would have accumulated guaranteed additions worth Rs 41.47 lacs.

If the last surviving annuitant passes away 5 years after the end of the deferment period, the investor would have got annuity payments for 5 years. At the time of demise, the nominee will get

Rs 10 lacs + Rs 41.47 lacs (accrued Guaranteed Additions) – 5*2.16 lacs (annuity payments already made) = Rs 40.67 lacs

The nominee can choose to receive the death benefit as lumpsum, immediate annuity or installments, as per his/her choice.

The Strange thing about LIC Jeevan Shanti

Ideally, with annuities, you would expect the annuity rate to increase with age.

However, if you look at the sample table (Option: 1: Deferred Annuity, single life), that is not always the case.

The annuity rate is, in a few cases, has gone down with an increase in the age of the annuitant. Do note this is happening only in case of deferred annuity variant (and not immediate annuity variant).

Why?

I think this is because there is death benefit involved. The death benefit is dynamic and will be greater than the purchase price, at least during the deferment period.

Death benefit = Purchase price + Guaranteed additions – Annuity payments already made.

Guaranteed additions, in turn, depend on the annuity rate.

Therefore, the death benefit will initially go up with time (till the end of the deferment period). Thereafter, it will come down as the annuity payments are made.

If the annuitant were to die early, the insurer has to make a significant pay-out (death benefit). Clearly, the insurance company will prefer if the pay-out does not happen soon.

If the annuitant were to die early, the insurer has to make a significant pay-out (death benefit). Clearly, the insurance company will prefer if the pay-out does not happen soon.

And the chances of an older man dying soon are higher. A lower annuity rate for such cases is a good way to lower your outgo (and perhaps good underwriting too).

I believe this is the reason why annuity rates in deferred annuity variants may go lower with age (if your entry age is beyond a certain threshold).

Now, the deferred annuity with joint life is likely to be even trickier. Since the death benefit is to be paid only after the death of the second annuitant, the annuity rate (keeping the age of first annuitant constant) will increase with the decrease in the age of the second annuitant.

So many factors at play.

By the way, the annuity rate will increase with the increase in the deferment period (for both immediate annuity and deferred annuity variants). The primary reason is that the payment (in higher deferment period option) will be delayed. Therefore, the time value of money reduces the insurer liability. In a lower deferment period option, the pension can start quite soon (and hence the insurer has to price annuity accordingly).

There is a good calculator for LIC Jeevan Shanti on this website. Though my calculations don’t exact match with the calculator, the numbers are quite close to give you an idea about how it works. You can even play around with the calculator and see how the mix of annuitants’ age and deferment period throws up interesting numbers.

LIC Jeevan Shanti: Tax Benefits

Investment under LIC Jeevan Shanti plan is eligible for tax benefit under Section 80CCC. Benefit under Section 80CCC comes under the overall limit of Rs 1.5 lacs under Section 80C.

The annuity income (pension income) is taxable at your income tax slab rate.

How to buy LIC Jeevan Shanti?

You can buy this plan by going to LIC branch or with the help of an LIC agent.

You can also buy LIC Jeevan Shanti plan Online. You have to go to the LIC website . As mentioned above, you will get a better annuity rate if you purchase the product online or if you are purchasing at the time of exit from NPS.

Should you invest in Annuity plans?

Not an easy question to answer. Let’s look at the pros first.

- By purchasing an annuity plan, you sell the longevity risk to the insurance company. The insurance has to make payments even if you live past the age of 150. An annuity purchase ensures that you never run out of money. Whether this amount will be enough is a different question.

- You pass on the interest rate risk to the insurance company. It is very much possible that the interest may go much lower in the future. You don’t have to worry. The insurance company bears the risk. You will get payments at the contracted rate.

- Easy to understand. Can be quite useful at an old age when your physical and mental abilities start deserting you. By the way, deferred annuity variant in LIC Jeevan Shanti is a bit tricky to understand.

There are quite a few cons too.

- The annuity rates tend to be quite low. The rates may be higher for options where there is no return of purchase price. However, in such cases, you must understand that the insurance company is making payments from your principal (since it does not have to return the principal).

- The annuity income is taxable at your marginal tax rate.

- The annuity income may not be inflation adjusted.

- You can’t exit (except for a few cases). Therefore, liquidity is an issue.

- You have to pay GST on the purchase price.

I have discussed these aspects in greater detail in this post.

Read: When to Purchase an Annuity plan?

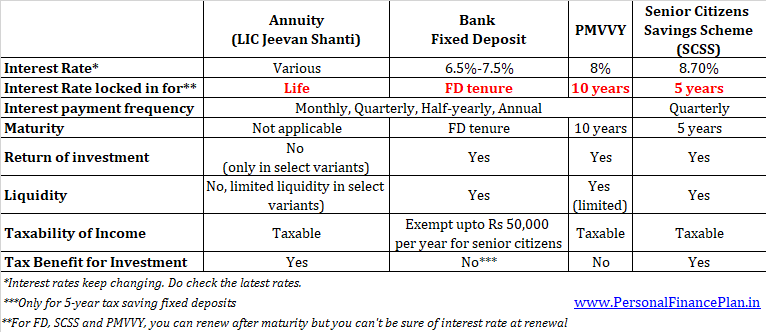

You also have to look at alternatives for generating income during retirement. You can invest in fixed deposits or debt mutual funds. If you are a senior citizen, you have additional options in Pradhan Mantri Vaya Vandana Yojana (PMVVY) and Senior Citizens Savings Scheme (SCSS).

You need to look at returns (interest rate), taxability and liquidity while making a choice.

Here is a brief comparison between LIC Jeevan Shanti, bank FDs, SCSS and PMVVY.

Do note it is not an either-or strategy. A smart retirement strategy may utilize a mix of these products.

What is good about LIC Jeevan Shanti plan?

- It is a non-participating plan. Therefore, there is no worry or uncertainty about the quantum of bonuses during the deferment phase.

- The annuity rate is guaranteed even for the deferred annuity plan. This is quite interesting.

- As an alternative to LIC Jeevan Shanti, you could have invested the amount elsewhere and subsequently used the accumulated amount to purchase an immediate annuity plan. However, in such a case, you wouldn’t have a guaranteed annuity rate. For all you know, the annuity rates may go down in the next 10-20 years.

- Therefore, everything is known upfront. You know upfront how much regular income you are going to get. This removes uncertainty about the annuity rate.

- With products such as National Pension Scheme (NPS) where there is a mandatory purchase of an annuity at the time of exit, a deferred annuity plan such as LIC Jeevan Shanti can be quite useful. If you don’t need regular income at the time of exit from NPS, you can pick up a deferred annuity (and choose deferment period accordingly).

From an investor’s point of view, this product is easy to understand.

In addition, it has all the benefits that an annuity plan has. I have covered such benefits of annuities in a previous section.

On the flip side, LIC Jeevan Shanti has all the flaws that an annuity plan has. In addition, the deferred annuity variants are not very easy to understand.

LIC Jeevan Shanti Vs. LIC Jeevan Akshay VI

- Both LIC Jeevan Shanti and Jeevan Akshay are single premium annuity plans.

- Both provide guaranteed income for life at the time of purchase i.e. you know upfront how much you will get for the rest of your life.

- LIC Jeevan Akshay VI offers you only immediate annuity option. On the other hand, LIC Jeevan Shanti offers you both immediate annuity and deferred annuity option.

- Under LIC Jeevan Akshay, a joint policy can only be purchased with the spouse. On the other hand, under Jeevan Shanti, you can purchase a joint policy with spouse, siblings or any lineal ascendant/descendant of a family i.e. grandparent, parent, children, grandchildren etc. Depending upon your family structure, LIC Jeevan Shanti offers you better flexibility.

- In case of annuity variants where annuity shall continue to the spouse, LIC Jeevan Akshay does not consider the age of the spouse. In the case of LIC Jeevan Shanti, the age of the spouse (or the second annuitant) is also considered.

The variants under immediate annuity plans are the same for both LIC Jeevan Shanti and LIC Jeevan Akshay plans. Therefore, if you have decided to purchase an immediate annuity plan from LIC, you simply need to compare the annuity rate for the desired variant under the two plans. Go with the plan that offers you a better annuity rate.

If you want to purchase deferred annuity plan from LIC, LIC Jeevan Shanti is your only option (between LIC Jeevan Akshay and LIC Jeevan Shanti).

Deferred Annuity Vs. Investing elsewhere, Use Proceeds to purchase an Immediate annuity

Let’s assume you are 50 years old. You need cash flow once you retire at the age of 60.

Assuming you want to take annuity route to generate cashflows, you have two options.

- Purchase deferred annuity today with a deferment period of 10 years

- Invest the amount somewhere. After 10 years, sell the investments and use the proceeds to purchase an immediate annuity plan

Under Approach 1, you invest Rs 10 lacs in LIC Jeevan Shanti-Deferred annuity-10 years. At the end of the deferment period, you will get an income of Rs 130, 824 per annum.

Under Approach 2, you invest the amount somewhere and use the proceeds from the sale of investment to purchase an immediate annuity plan after 10 years.

Assuming the immediate annuity rates remain constant, for you to earn a pension of Rs 130,824 per annum, you need Rs 14.38 lacs at the end of 10 years.

How did I arrive at Rs 14.38 lacs?

130,824/90,942*10 lacs = 14.38 lacs, For age 60 and immediate annuity without return of purchase price (Option A), the corresponding value is Rs 90,942.

Now, for Rs 10 lacs to grow to Rs 14.38 lacs in 10 years, you need a post-tax return of 3.7% p.a. Should be easy to achieve.

Even if you were to purchase annuity without return of purchase price (Option F) at the end of 10 years (and get annual pension of Rs 130,824), you would need Rs 19.3 lacs.

130,824/67,482* 10 lacs = 19.3 lacs

Annuity value for Rs 10 lacs purchase, 60 years, Immediate annuity with return of purchase price = Rs 67,482

To get to Rs 19.3 lacs in 10 years, you need post-tax return of 6.8% p.a. Not very difficult again.

However, the caveat is that the immediate annuity rates may change over the next 10 years. If the annuity rates move lower in the interim, you need a much larger corpus to achieve the same level of income. For a larger corpus, you need higher returns.

Therefore, Approach 1 provides guaranteed pension while Approach 2 carries some risk.

Are you willing to take such a risk?

Which variant of LIC Jeevan Shanti should you opt for?

Assuming you have decided to go with an annuity plan, you still need to select the annuity variant.

The choice between immediate annuity plans is relatively simpler.

It will depend on your requirement.

If you want to leave a legacy for your family, you should consider Option F and J.

If you want to ensure pension for your spouse too, consider Options H, I or J.

If you want your annuity pay-outs to grow gradually, you may opt for Option G.

If you want higher income but want to ensure cashflows to the family for a minimum period, Options B/C/D/E may be the right choice for you.

If you merely want to maximize income (and are not concerned about leaving a legacy), you may like Option A the most.

However, in my opinion, the choice between the deferred annuity variants is quite complex. Since the death benefit is dynamic and the age of the second annuitant also matters, there are so many permutations and combinations I can think of.

For instance, if you are 60 and want to purchase a plan with deferment of 10 years (Option 1, single life), you will get an annual pension of Rs 1.37 lacs (after the end of deferment period).

However, if you were to add a second annuitant (aged 30) in the same plan (Option 2, joint life), you will get an annual pension of Rs. 1.2 lacs.

So, a higher pension under Option 1.

If the deferment period were to be increased to 20 years, you will get a pension of Rs 1.49 lacs under Option 1 and Rs. 2.19 lacs under Option 2. Now, higher pension under Option 2.

Complicated, isn’t it?

Which variant will you choose?

We have discussed only deferred annuity variants earlier. The immediate annuity variants are explained with illustrations below.

LIC Jeevan Shanti: Option A (Immediate Annuity)

Annuity for Life

Immediate annuity, single life

Pension Benefit: You will get pension throughout life. Pension will stop after your death.

Death Benefit: Nominee will not get anything after demise of the annuitant. Payment of pension will also stop.

Maturity Benefit : Not applicable

Surrender Benefit : Not allowed. This means that you or your nominee will never get the invested amount back.

The annuity rates are the highest under this option because the insurer has to pay only till the end of purchaser’s life. No payments (lumpsum or annuity) to be made after investor’s demise.

Example

A 60 year old person invests Rs 10 lakh in Option A. The total outgo will be Rs 10.18 lacs (inclusive of GST).

If you look at the corresponding age and option (i) in the table, you will find 90,942.

This means you will get Rs 90,942 per annum.

You will get this pension for life. Pension will stop after your death. No annuity or lump sum will be given to your spouse or nominee.

In case of an early death, your money goes to the sink. For instance, if the investor dies after two years, he would have got pension of only Rs 1.82 lacs (90,942 X 2). Nothing will be given to spouse or nominee after the demise of the investor.

LIC Jeevan Shanti: B/C/D/E (Immediate Annuity)

Annuity payable for 5, 10, 15 or 20 years certain and thereafter as long as the annuitant is alive.

Immediate annuity, single life

Under this variant, you can choose from 4 options for Guaranteed period: 5 years, 10 years, 15 years or 20 years

Pension Benefit :

You will get pension for life.

If you pass away before the end of the guaranteed period, the nominee will get the pension till the end of the guaranteed period. The pension to the nominee will stop at the end of the guaranteed period.

If you pass away after the expiry of the guaranteed period, the pension will stop after your demise. Nothing will be paid to your nominee.

As expected, the lower the guaranteed period, the higher the interest rate.

Death Benefit: No lumpsum payout shall be made to the nominee after demise of the investor. As mentioned above, if the purchaser were to die before the end of guaranteed period, the nominee will get the pension till the end of such period.

If the investor passes away after the end of guaranteed period, the nominee gets nothing.

Maturity Benefit : Not applicable

Surrender Benefit : Not permitted

Illustration

A 60 year old person invests Rs 10 lakh in Option D (15 years). The total outgo will be Rs 10.18 lacs (inclusive of GST).

From the table (60 years and option ii), you can check that the corresponding value is Rs 86,250. For an investment of Rs 10 lacs, you will get an annual pension of 86,250 rupees.

You will get this pension for your entire life.

But if you die after 6 years, then your nominee will get pension for the remaining 9 years (15 years – 6 years). Pension to the nominee will stop at the end of guaranteed period.

If the you pass away after 15 years (end of guaranteed period), then the pension will stop after your demise. Your nominee will not get anything.

LIC Jeevan Shanti: Option F (Immediate Annuity)

Annuity for life with return of purchase price on the annuitant

Immediate annuity, single life

The only difference between Option A and Option F is that, under Option F, the purchase price is returned to the nominee. Since the liability of the insurer is higher under Option F, the annuity rate is also lower (as compared to Option F)

Pension Benefit: You will get pension for life. Pension will stop after your death.

Death Benefit: On the death of the investor, the payment of pension will stop and the investment amount will be returned to the nominee. If you had invested Rs 10 lakh, then 10 lakh rupees will be returned to the nominee. GST charged at the time of will not be returned.

Under Jeevan Shanti, the nominee has the option to get the death benefit as lump sum. Or he can use the death benefit amount to purchase an immediate annuity plan. Or he can choose to receive the benefit in the form of monthly/quarterly/half-yearly/annual investments over 5, 10 or 15 years. LIC Jeevan Akshay provides the option of only lump sum.

Maturity Benefit: Not applicable

Surrender Benefit: You can surrender the policy one year after taking the policy.

Surrender Value will depend on your age at the time of surrender. I am not sure how to calculate this amount.

Illustration

A 60 year old person invests Rs 10 lakh in Option 3. The total outgo will be Rs 10.18 lacs (inclusive of GST).

From the table, you can check that the corresponding value (60 years and Option iii) is Rs 67,482. For an investment of Rs 10 lacs, you will get an annual pension of 67,482 rupees.

You will get the pension for life. Pension will stop after your death.

10 lakhs will be returned to your nominee on the amount of death. Alternatively, the nominee can choose to purchase an immediate annuity with the amount or the receive the benefit in installments.

LIC Jeevan Shanti: Option G (Immediate Annuity)

Annuity payable for life increasing at a simple rate of 3% p.a.

Immediate annuity, single life

Pension Benefit: You will get pension for life. Your pension will increase by 3% every year.

Death Benefit: On the death of the investor, the pension (annuity payments) will stop. Nominee will not get anything.

Maturity Benefit : Not applicable

Surrender Benefit: Not permitted

Illustration

A 60 year old person invests Rs 10 lakh in Option G. The total outgo will be Rs 10.18 lacs (inclusive of GST).

For an investment of Rs 10 lacs, you will get a pension of Rs 72,888 in the first year.

In the second year, the pension amount will increase by 3% i.e. Rs. 75,074

In the third year, the pension will increase to Rs. 77,261.

Similarly, the pension amount will continue to rise throughout your life.

Pension will stop after your death. Your nominee will not get anything back.

LIC Jeevan Shanti: Option H (Immediate Annuity)

Annuity for life with a provision of 50% of annuity payable to spouse during his / her life on the annuitant

Immediate annuity, Joint Life

Pension Benefit: The investor will get pension for life. After the death of the investor, the spouse will get pension for his/her life. However, the spouse will get only 50% of the pension amount (that was being paid to the investor).

Death Benefit: 50% of the pension will be paid to the spouse on the death of the investor.

After the demise of the spouse, the pension will stop and the nominee will not get anything.

If the spouse passes away before (predeceases) the investor, the pension will stop after demise of the investor. Nominee will not get anything.

Maturity Benefit: Not applicable

Surrender Benefit: Not permitted

Illustration

A 60 year old person invests Rs 10 lakh in Option H. The total outgo will be Rs 10.18 lacs (inclusive of GST).

The corresponding value in the table for the age of 60 and Option H is 85,638.

You will get this pension for life. After you, your spouse will get half this amount for life i.e. your wife (or husband) will get an annual pension of 85,638 * 50% = 42,819.

After the death of your spouse, pension will stop. Nominee will not get anything.

If your spouse predeceases (passes away before) you, the pension will stop on your demise. Your family or nominee will not get anything.

LIC Jeevan Shanti: Option I (Immediate Annuity)

Annuity for life with a provision of 100% of annuity payable to spouse during his / her life on the annuitant

Immediate annuity, Joint Life

Only a minor difference as compared to option H.

Under Option H, after investor’s demise, the spouse got 50% pension for life.

Under Option I, after investor’s demise, the spouse will get 100% pension for life.

Since the liability of the insurance company is higher under Option 6, the annuity rate for Option 6 is lower as compared to Option 5.

Illustration

A 60 year old person invests Rs 10 lakh in Option 6. The total outgo will be Rs 10.18 lacs (inclusive of GST).

The corresponding value in the table for the age of 60 and Option I (or option vi) is 80,844.

For an investment of Rs 10 lacs, you will get a pension of Rs 80,844 per annum.

You will get this pension for life. After you, the exact same pension will continue to your spouse. Your wife (or husband) will get an annual pension of Rs. 80,844.

After the death of your spouse, pension will stop. Nominee will not get anything.

If your spouse predeceases (passes away before) you, the pension will stop on your demise. Your family or nominee will not get anything.

LIC Jeevan Shanti: Option J (Immediate Annuity)

Annuity for life with a provision of 100% of annuity payable to spouse during his / her lifetime on death of the annuitant. The purchase price will be returned to the nominee

Immediate annuity, Joint Life

Under Option I, the family gets nothing after the demise of husband and wife.

The difference in option J is that after the death of husband and wife, the investment amount is returned to the nominee.

Pension Benefit: The investor will get pension for life. After the death of the investor, the spouse will get the 100% pension for his/her life.

Death Benefit: 100% of the pension will be paid to the spouse on the death of the investor. Under Jeevan Shanti, the nominee has the option to get the death benefit as lump sum. Or he can use the death benefit amount to purchase an immediate annuity plan. Or he can choose to receive the benefit in the form of monthly/quarterly/half-yearly/annual investments over 5, 10 or 15 years. LIC Jeevan Akshay provides the option of only lump sum.

After the demise of the spouse, the pension will stop and the nominee will be given back the investment amount.

If the spouse passes away before (predeceases) the investor, the pension will stop after demise of the investor. The investment amount will be returned to the nominee.

Maturity Benefit: Not applicable

Surrender Benefit: Not permitted

Illustration

A 60 year old person invests Rs 10 lakh in Option J. The total outgo will be Rs 10.18 lacs (inclusive of GST).

The corresponding value in the table for the age of 60 and Option J (or option vii) is 67,074.

For an investment of Rs 10 lacs, you will get a pension of Rs 67,074 per annum.

You will get this pension for life.

After you, the exact same pension will continue to your spouse. Your wife (or husband) will get an annual pension of Rs. 67,074.

After the death of your spouse, pension will stop. Your nominee will get Rs 10 lacs.

If your spouse predeceases (passes away before) you, the pension will stop on your demise. Your nominee will get Rs 10 lacs. Alternatively, the nominee can choose to purchase an immediate annuity with the amount or the receive the benefit in installments over 5/10/15 years.

Additional Links/Source

- HDFC Life Sanchay Plus: Review

- HDFC Life Pension Guaranteed Plan Vs. LIC Jeevan Shanti

- LIC Jeevan Akshay VI

- LIC New Money Back Plan-25 years

- LIC Children’s Money Back Plan

- LIC Jeevan Tarun

- LIC New Endowment Plan

- LIC Jeevan Labh

- LIC Bima Bachat

- LIC Jeevan Umang

- LIC Jeevan Utkarsh

- LIC Jeevan Shiromani

- LIC Bima Shree

- LIC Single Premium Endowment Plan (Table no 817)

- Problems with Endowment Plans

- With Traditional plans, age affects your returns

36 thoughts on “LIC Jeevan Shanti (Plan 850): Single Premium, Guaranteed Pension (Features and Review)”

Under option G (immediate annuity), annuity increases by a simple rate of 3%. However, from the annuity for third year in your illustration, it appears that the annuity increases at a compounded rate of 3%. Kindly clarify.

Thanks Mahavir for pointing out. Corrected now.

I have moved to canada on 9th July 2015 as a Permanent Residence. and my present status is NRI. I am planning to get my canadian citizenship in 2019 and then move to india as resident.Please clarify if I am eligible for LIC Jeevan Akshay VI on line .

If you cease to be an Indian citizen,

I don’t think you can purchase plans from LIC., you can still purchase plans from LIC.Suggest you go through this link.

https://www.licindia.in/Customer-Services/NRI-Center

Refer to part B of the link.

However, I am not sure as the language is not very clear.When you return to India, you will be an Indian resident and a Canadian citizen. This may change the equation. Please check with LIC.

EXCELLANT ANALYSIS. EVEN COMPARED SCHEME WITH BANK FD, SCSS, etc..THANKS A LOT.

DEEPAK

You are welcome, Deepak!!!

Please share with your friends and family too.

I’m very confused by seeing all these options.

As a analyst, i request you to reply personally which option gives more benefit in immediate or deferred plan. And also reply single or joint option, which one is good

Ravi,

If you are sure you need to purchase an annuity plan:

1. if you need regular income to start right away: pick an immediate annuity

2. If you want income to start after some time: pick a deferred annuity

The choice between the various variants is not that simple.

Not possible to comment without knowing about your family structure and requirements.

Thanks for your kind reply…

and my age is 37 and my spouse age is 28.

I like to invest Rs.5 Lakh.

I wish to know, which annuity plan is more ‘profitable’.

Pls Reply

Hi Ravi,

At your age, you shouldn’t be looking to invest in an annuity plan.

It is really a very good analysis. My age is 44 and my spouse is 35. I am interested for deferred annuity. Please suggest which option suits me better ? Thanks in advance.

Hi Sudip,

It is difficult to comment. Depends on your family structure and how you think annuity fills a purpose in your overall plan.

A few pointers:

If you want pension to continue to your spouse too, you can think of joint life option. However, pension to the spouse can be managed in many other ways too.

Thanks for the information. What is the yield (return on investment) under various plans?

Hi Chintan,

Since the cash flows are indeterminate (depends on how long you live), it becomes a complex exercise.

However, you can assess for the variants with the return of purchase price. For immediate annuities (return of purchase price), it will be rate of interest offered.

HI : for an Insured who has purchased term plan, undergoes a surgery after 2 yrs of purchase of plan – should the insured inform the term plan insurance company about the surgery – what are dos and donts, and what are the impacts

Regards

Vipin

No need to inform insurer.

Dear sir,

Details:- NPS subscriber, premature exit from central govt.

DOB- 01 Jan 1988, Purchase price 6.5 lekh

You have suggested to purchase the Jeevan Shanti of LIC. But I have found that annuity amount is high with ICICI Prudential to compare other ASPs like Lic, Hdfc, and Sbi. So I confused. Please guide me.

I also want to know that, after purchasing annuity, Will regular income (monthly pension) start same time or after some years.

GO with the insurance company that offers the best interest rate.

Jeevan Shanti gives the benefit of the deferred annuity.

Pls tell , what will happen if nominee under option j (immediate annuity) dies during the policy period. Can we change the nomination later on .

Excellent Analysis. Online policy provides additional benefit of 2% of annuity amount . Will it be applicable even if choose Option J immediate annuity , monthly mode of annuity ? This benefit applicable to only first year (or)thru out the payout years. Many thanks in advance.

Thanks Sreenivas.

Yes, the premium is slightly lower if you purchase the plan online. The premium has to be paid just once.

Dear Sir, Can you please clarify on the clause mentioned for Jeeven Shanti Policy from LIC website :

As per LIC Website , it says :

Surrender Allowed: The policy can be surrendered at anytime after three months from“ the completion of policy “when Annuity Option is with return of purchase price.

What is meant by completion of policy ? If one chooses immediate annuity plan and say after one year, want to surrender , is it possible ? Any deductions? Technically it is not completion of policy, as the annuity is valid for life under Option J.

Kindly advise.

I am 86 which option is more suited. May be immediate annuity since I need regular money for maintenance.for me my wife .Thanks for your guidance if forthcoming.

Dear Sir,

It is a difficult question to answer. I need much more info about you before I can answer this question.

You have to weigh between liquidity and income.

Annuity without the return of purchase price will provide you a very high income. The problem is that nothing gets passed on to your nominee after you.

Here is what you can consider.

Keep sufficient money aside for emergency.

Purchase annuity (without the return of purchase price) for your mandatory expenses. You will divide the purchase amount between you and your spouse.

Any mismatch in the cashflows can be bridged through FD, PMVVY and SCSS interest.

Sincerely appreciate the evident extra effort you have put in replying to senior citizen.

Hope karma pays you well. Best wishes!

Sir,

I am now 60. I want to purchase a joint life deferred (5years) Jeevan Shanti (Plan 850) annuity plan with my wife. My question is 1) if any one of the two dies in the period of deferment can the surviving one continue the plan or surrender it?

2) Can the policy be surrendered at any time after 3 months of purchase. If it is true then whether both the survivors have to sign the surrender form?

3) What is this “SURRENDER VALUE”? Is there any deduction from the original purchase price? OR there are some additions to it?

Sir, What is the variance of annuity rate one would get if he/she is 52 and investing online for an immediate annuity rather than the normal route ?

Thanks

Best Regards

R. Misra

Everything else being the same, you will get 2% more pension for online purchase.

Detailed and in depth analysis, like always. One more important thing, easy to understand and take decisions.

Thanks!!!

Is monthly pension given by LIC after deducting ‘Income Tax’? Regards.

What is the rate of return? Is it fixed for all the return years or varies?

Dear Sir

It is very good analysis.But i have confused with different variant. Pl guide my to my personnel my clarification.

I am 60 years and my wife is 58 years. Both are getting pension from central government. Can u please guide me which variant i should take. I want to invest 5 lakhs to 10 Lakhs.

Regards

KRISHNAN

Hello Sir,

Thank you for the analysis and enlightenment.on this sensitive yet important matter.

I am 56. I need an annuity from 58 or 60 for 10-12 years with return of purchase price and also with loan or surrender options. Currently I am holding a Jeevan Anand policy plan 149 bought in 2008 and maturing in 2021. To gather enough money for the SP for annuity I am planning to commute the death benefit of Anand-149.

1..Which option is the best one for me considering least risk, ROI and above sought options. I am free to opt for Banks, LIC etc.

2..Is it advisable to commute the death benefit of 149 plan. I will get about one third of the benefit if I commute on maturity. I have a different plan for security of the spouse.

Thank you sir,

My kindest regards,

Mohammed

Hi Deepesh –

Is Jeevan shanti plan getting closed by 20 Oct, next week? any updates on this please.

What was the rate of monthly interest of Jeevan Shanti (850) Deffer Period 2 Years.

I took policy on 24.09.18 What will be the pension.