LIC has launched two new Unit-Linked Insurance Plans (ULIPs) in March 2020, LIC Nivesh Plus (Plan 849) and LIC SIIP (LIC Systematic Investment Insurance Plan, Plan 852).

LIC is a behemoth in traditional life insurance plans and has not been very active in the unit-linked products space. The private insurers have been super-active in the ULIP space and have shown a fair amount of product innovation in their ULIP products. The costs have come down, which is a good development for the investors. As I see, LIC now wants to catch up with the private insurers.

In this post, let’s find out more about the LIC Nivesh Plus plan.

LIC Nivesh Plus Plan (Plan 849): Salient Features and Review

- It is a unit-linked insurance plan (ULIP). This means there is no guarantee of returns.

- This is a Type I ULIP. At the time of demise, the nominee gets Higher of (Sum Assured, Fund Value). Under a Type II ULIP, the nominee gets Sum Assured + Fund Value. Everything else being the same, Type I ULIP provides better returns while the Type II ULIP provides better life cover.

- Single Premium plan (you need to pay the premium just once)

- Sum Assured: You have two choices. The option once chosen cannot be changed. This choice has very important tax and return implications. Will discuss this later.

- Option 1: 1.25 times Single Premium

- Option 2: 10 times Single Premium

- Policy Term: Can range from 10 to 25 years, depending upon your age and Sum Assured option chosen.

- Eligibility: I reproduce an image from the product brochure

- Charges in the plan: You have usual suspects. Premium allocation charges, Mortality charges, fund management charges, switching charges, partial withdrawal charge etc. Will discuss these later in the post.

- You CAN NOT get a loan under LIC Nivesh Plus plan. Loans are not permitted for ULIPs.

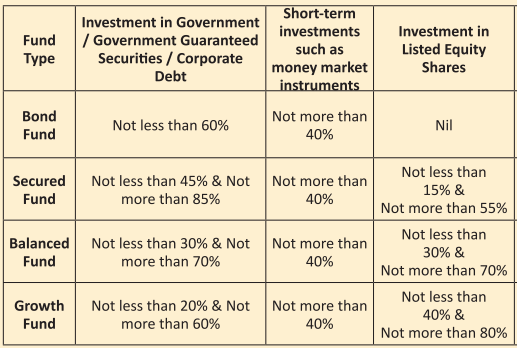

- You have 4 fund choices

LIC Nivesh Plus (Plan 849): The Charges and the impact

For a deep dive into various types of charges in ULIPs, how they are adjusted and their impact on returns, refer to this post.

The ULIPs have the same nomenclature for the charges. I will point out areas where LIC Nivesh Plus is better or worse than other popular ULIPs.

Premium allocation charge: This charge is deducted from the premium before your money gets invested. GST is also applicable on these charges.

In LIC Nivesh Plus, Premium allocation charge is

- 5% for offline sales (through agents)

- 5% for online sales (through LIC agents)

Therefore, if you invest Rs 10 lacs in the plan, Rs 41,300 (incl. 18% GST) will be charged in case of offline purchase and Rs 17,700 (incl. 18% GST) in case of online purchase. This money is just gone.

At a time when private insurers are moving towards zero premium allocation charge at least for online sales, these charges are atrocious.

Mortality charges: These charges go towards providing you the life cover. The mortality charges depend on your age and are recovered every month through the cancellation of fund units every month. I reproduce the mortality charge table from the policy wording document on LIC website.

Mortality charges increase with age. So, if you are old, mortality charges will affect your returns more. At the same time, since this is a Type I ULIP (sum-at-risk = Sum Assured – Fund Value), the impact of mortality charges will be lower.

However, if you have chosen the Sum Assured as 10 times Single premium, the mortality charges will simply destroy your returns (more on this later).

I found the charges slightly higher than some of the ULIPs from private companies that I looked at.

LIC Nivesh Plus: Which Sum Assured Option should you choose?

This is very interesting. LIC Nivesh Plus is a single premium plan. Single Premium plans have a unique tax problem.

We all know that life insurance proceeds are exempt from tax. Yes, mostly but that’s not always the case. For maturity proceeds to be exempt from tax, the Sum Assured should be at least 10 times the annual (or single premium). If this condition is not met, the maturity proceeds are taxable. There is TDS of 5% too.

Under Option 1 (Sum Assured is 1.25 times single premium), this condition is not met. Therefore, maturity proceeds will be taxable.

Under Option 2 (Sum Assured is 10 times single premium), this condition is met. Therefore, the maturity proceeds will be exempt from tax. However, since Sum-at-Risk is very high, mortality charges will heavily eat into your returns.

Let’s understand this with the help of an example. LIC has made my task easier. I reproduce illustrations from the product brochure.

Pulkit is 30 years and invests Rs 1 lac in this plan.

The illustrations show returns for gross investment returns of 4% and 8% p.a. (as mandated by IRDA). Being a ULIP, you would expect the investments to earn a higher return but that’s not important right now. The returns will also depend on your age and the funds chosen.

Let’s first look at the Option 1.

As per the illustration, if Pulkit invested in the 20-year policy, he would end up with Rs 3.53 lacs at the end of 20 years (assuming gross returns of 8% p.a.). That is a net return of 6.51% p.a. 1.49% p.a. knocked off. Where did the money go? Towards various kinds of charges.

If your net return was 8% p.a. on this investment, you would have ended up with Rs 4.66 lacs. This means charges wipe off almost 31% of the gross returns.

You must note that this money is taxable.

Now, to option 2 (Sum Assured is 10 times the Single Premium)

Pulkit ends up with Rs 2.67 lacs (at 8% p.a. gross returns). That is much lower than Rs 3.53 lacs in Option 1. Under Option 2, your net return is 5.05% p.a. (was 6.51% under Option 1). That’s 2.95% p.a. shaved off the gross return. Charges wipe off almost 55% of the gross returns.

Why this difference?

Mortality charges will be way higher since the Sum Assured is 10 lacs (10 times Single Premium). Under option 1, the Sum Assured will be Rs 1.25 lacs.

The only solace is that these proceeds will be exempt from tax.

Points to Note

- Everything else being the same, you will end up with a higher corpus under Option 1 (compared to option 2). The Life cover will be lower. The maturity proceeds will be taxable.

- Everything else being the same, you will end up with a lower corpus under Option 1. The Life cover will be higher. The maturity proceeds will be exempt from tax.

- Option 1 (Sum Assured is 1.25 times single premium): Better Returns. Lower Life Cover. Maturity Proceeds taxable

- Option 2 (Sum Assured is 10 times single premium): Inferior Returns. Higher Life Cover. Maturity Proceeds exempt from tax

- Death benefits will be exempt from tax in both cases.

- If gross returns are higher or lower than 8% p.a., your net returns will also be higher/lower.

- The returns also depend on the age of the investor. If Pulkit was 35, the returns will be even lower.

- For Option 1, the tax benefit under Section 80C will be capped at 10% of Sum Assured. So, if you invest Rs 1 lac, the Sum Assured will be Rs 1.25 lacs. The tax benefit under Section 80C will be 12,500 (10% of Sum Assured).

What about Guaranteed Additions?

The plan provides guaranteed additions too (kind of loyalty benefits).

As always, this is pure nonsense. Everything comes from your money (from all the charges that they have collected). This is nothing more than a marketing gimmick.

LIC Nivesh Plus: Should you invest?

My answer is No. I recommend that you keep your insurance and investment products separate. You will be better off buying a term plan and investing in pure investment products such as PPF, mutual funds etc.

However, if you must invest in this plan (many investors can’t simply say No to LIC), do think through the Sum Assured choices and their return and tax implications.

Additional Read/Source

- LIC Nivesh Plus (Plan 849): Product Brochure

- LIC Nivesh Plus (Plan 849): Policy wordings

- LIC Nivesh Plus page on LIC website

- How to select the Best ULIP?

- Why I prefer Mutual Funds over ULIPs?

- ICICI Prudential Life Signature ULIP

- How various charges in ULIPs destroy your returns?

- In a ULIP, you pay more for the life cover as compared to Term Life Insurance Plans

- In traditional plans and ULIPs, your age affects your returns

- The problem with Single Premium Life Insurance Plans

- The Entire Life Insurance Premium is not tax deductible

- If you are old, don’t buy ULIPs

3 thoughts on “LIC Nivesh Plus (849): A New ULIP from LIC: Review”

I think buyers of this ULIP will get the cool Yes Bank shares at RS.1 each.

What thrilling investment!!!

🙂

The allocation charges in LIC Nivesh Plus is 3.3% and not 5% as you mentioned.

Why should insurance be sold offline?